Cloud Wars: Who's Winning and why it doesn't Matter

What is the industry response to the AWS advance?

Meanwhile, IBM, HP, Microsoft, the EMC/VMware federation and other incumbents have taken notice and are investing heavily in new technology to help customers simultaneously achieve the business benefits of cloud computing, minimize migration risk and maintain platform stickiness. Case in point is ...

Nine years of cloud computing and counting...

The year was 2006. While Andy Jassy and Jeff Bezos were inventing a whole new way of delivering technology over the Internet at Amazon, I was busy at HP trying to convince customers to move their applications from legacy IBM mainframe systems to UNIX systems. As you might guess, that didn’t go too well; I was stunningly unsuccessful convincing folks to move off mainframes. (Fortunately, I could consistently beat quota by helping customers deploy standard UNIX workloads like Oracle and SAP.) The re-platforming cost and risk was just too great and an IBM sales rep would always come in at the 11th hour with a low-ball offer and a reminder of the risk and lack of experience with the new platform - and the deal died. I learned an extremely important lesson from that experience:

Don’t underestimate the power of those leveraging resistance to change

Fast forward to 2015 and the IT technology world is radically different, but some things haven’t changed. Although declining gradually, IBM’s mainframe ecosystem is still generating billions in revenue. Corporate IT is now largely virtualized but most application architectures are unchanged from when they ran on physical servers. Companies like Uber, Airbnb, and Netflix that were “born in the cloud” are disrupting their respective industries with technology from Amazon, Google and others, but over 90% of the Gartner estimated $3.8 trillion in 2015 worldwide IT spend will still be on legacy systems and services to support those systems. Why?

The answer is that most technology decisions are rational and those decisions depend on both the value and cost of changing technology. More on the value part of the cloud equation and why many companies are missing the point in a future post.

What is the industry response to the AWS advance?

Meanwhile, IBM, HP, Microsoft, the EMC/VMware federation and other incumbents have taken notice and are investing heavily in new technology to help customers simultaneously achieve the business benefits of cloud computing, minimize migration risk and maintain platform stickiness. Case in point is IBM's acquisition of and further investments in Softlayer while rumors swirl about reducing overall headcount. Many of us recognized the same pattern in the early 2000’s when leading telecommunications providers maintained their status as incumbents by turning a potentially disruptive new cellular technology into a way to combat new entrants, an approach described in Clayton Christensen's book, Innovator's Solution.

The idea is that current leaders can minimize disruption if they recognize the threat early enough and invest aggressively in new technologies and business methods to protect their industry position, even though new players are deploying new technologies in a way that disrupts the industry's predominant business model. Oftentimes, this requires carefully staged self-cannibalization. HP, for example, addressed this by keeping its cloud services organization separate from its enterprise services business unit (the old EDS business).

How is cloud computing disrupting the IT sector?

The pattern we are seeing in cloud computing at the moment doesn’t fit the classic industry disruption model. Unlike their colleagues in the retail and media sectors, IT industry leaders are fighting back by evolving their business models, making new investments and rapidly co-opting new technologies.

By some, this could be seen as a provocative statement

Is the growth of cloud computing disruptive? Absolutely, but it depends on your perspective of who is being disrupted. We can expect to see continued turbulence where a number of IT companies will not navigate the transition to the as-a-service cloud business model, but most of the biggest players will be able to maintain their position as industry leaders (although the order will likely change in the shakeout)

Traditional IT leaders are starting to see the results of their cloud efforts

As we see IT industry incumbents invest heavily in new capabilities and technologies and co-opt cloud innovation concepts, we are also seeing them aggressively work to maintain and extend their platform ecosystems. Those efforts are starting to generate results. By some measures, Microsoft is growing its cloud revenue almost twice as fast as Amazon, and IBM is only 2 percentage points behind.

Case in point: Even though Amazon AWS is the clear market leader with up to 75% share of cloud platforms according to Forrester, Microsoft has grown its cloud business from low single digit market share 3 years ago to as high as 25% at the end of 2014.

This is because of the mature Microsoft ecosystem combined with the gradual maturation of Microsoft cloud technologies. The key word here is ECOSYSTEM. Microsoft has 10,000’s of partners, a large mature enterprise sales force and a .NET platform that is nearly ubiquitous with Fortune 1000 IT departments. Because of this, they can leverage the high ground to gain cloud market share from AWS, Google and other new entrants and protect their base. Other leaders like EMC and IBM are employing a similar strategy. Does this mean that IBM and the other incumbents are out of the woods? No, but they're fighting back hard and aren't going anywhere anytime soon.

The Cloud Biome: A set of ecosystems emerge

While the new players led by Amazon and Google are growing their cloud ecosystems organically, established players are re-purposing their existing ecosystems of developer communities, resellers, technology providers, integrators, and service providers. This takes work: There are new winners and losers and capabilities have to be evolved but the results are unmistakable. Taking a closer look, we see a key subset of cloud platform ecosystems emerge:

- Amazon AWS

- Openstack – IBM, HP, Red Hat, Rackspace

- Microsoft Azure

- VMware/EMC

Other platforms may achieve critical mass in the future, but it’s clear these platforms are here to stay. One way of looking at this is to look at the number of jobs posted requiring competence with a particular platform. If you look at trends on the Indeed.com website, you will see skills related to all of these platforms in high demand. (Be careful how you read the results though, the high growth of jobs in the transportation sector skews the results.)

Do enterprises care who’s the biggest? No.

Every platform mentioned here has and will continue to attract its share of customers for the foreseeable future. Many enterprises will also standardize on multiple platforms depending on their current state, future state plans, and to spread out risk. Do we care which platform provides the best fit for any given situation?

Absolutely yes, but.....

I’d love to hear your thoughts; let me know what you think by leaving a comment below.

The “Chasm” between Technology Convergence and Business

I recently came across Geoffrey Moore's recent YouTube video, Is Your Business Model Being Disrupted? The Era of Code Halo... and it triggered a few thoughts....

Originally posted on www.tylerjohnsonconsulting.com.

I recently came across Geoffrey Moore's recent YouTube video, Is Your Business Model Being Disrupted? The Era of Code Halo... and it triggered a few thoughts.

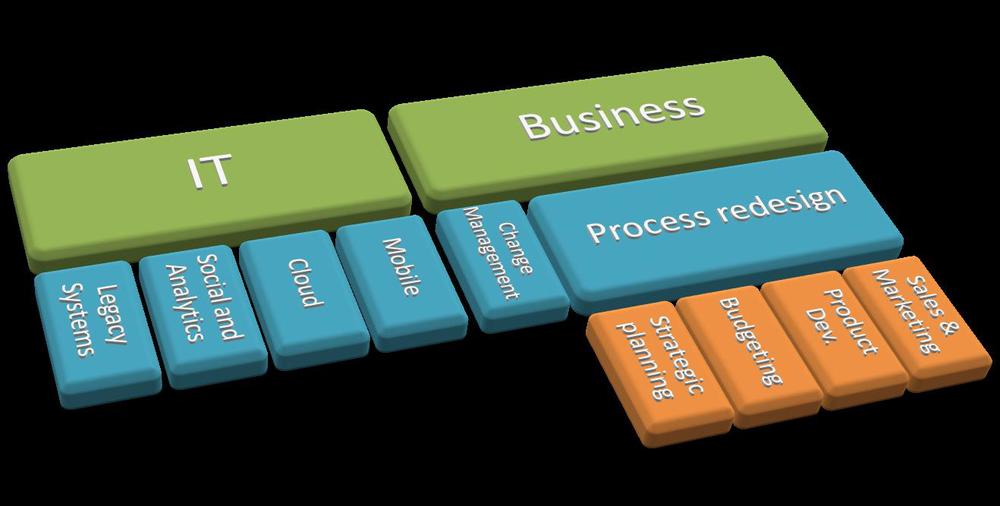

First, I think Geoffrey Moore and guest Malcolm Frank, author of book on Code Halos or “digital footprints” are definitely on the right track on their thinking around SMAC – “social, mobile, analytics, cloud” (And I will buying and reading the book – unless someone wants to send me a free copy…). Gartner calls it "Nexus of Forces" – another term I’ve heard is technology convergence. The reality is that these new technologies in various ways are being used to create new business models that are disrupting every industry from publishing to retail and beyond.

In particular, I like this framework from the video: (Let’s call it “Geoffrey’s SMAC down”.)

What we are talking about is adoption of these radically new technologies as a weapon to disrupt your industry. The massive challenge here (as discussed in the video) is that this framework represents pulling together a daunting set of skills and knowledge that few companies have in house. Sounds like an opportunity for consultants, right? While that may be true, (Moore and Frank are consultants after all J) that’s just the beginning. IT and business executives will need to develop new skills, new business processes have to be developed and implemented, organizational evolution will need to occur. You could hire Chasm, or Cognizant, or KPMG, or Deloitte, but I don’t believe that is enough if you’re the right people in your organization don’t understand the interplay between technology and business in this context. Change is hard because it requires making the right investments and right tradeoffs in the right places; this is why most industries will eventually be disrupted by new entrants with only few surviving incumbents. To understand this more fully, let me take you through a thought experiment.

Let’s look at a hypothetical large retail banking institution. The IT folks are thinking about virtual desktop (VDI) solutions as a way to reduce cost, improve security. Leadership is thinking about their M&A strategy, litigation, and growing profits. How could VDI transform their business?

· M&A – grow revenue be accelerating integrations, make acquisitions more accretive. How? By deploying VDI, the bank could move an acquisition’s remote offices’ core banking software over instead of integrating two systems and replacing all the local PCs. (They probably need a private cloud solution as well)

· Litigation – total control over all data by not letting it leave the datacenter. This reduces the risk of employees stealing customer data, hacking/tampering with software installed at the remote office, etc.

· Profit – reduce cost of building and supporting new remote locations. Enable new form factors for remote locations. Remote tellers? (Implies linkage with a mobile strategy)

Unfortunately, each group has their own POV and has a hard time communicating their needs and the implications of their needs to the other. As a result, communication reduces down to the lowest common denominator – “cost reduction”. They’re using the current budgeting process. Based on NPV, EVA, payback, etc., this process doesn’t take into account the other benefits of a VDI solution. They need a new way to prioritize investments; soft benefits need to quantified, which requires understanding of both the technology and the business impact of the technology, not an easy task. To trust the process, producers and consumers of the analysis need to understand both the technological and business implications of the transformation. The organization itself needs to change, i.e. what organization, roles, and skills are required to successfully complete such an exercise? You could argue that you just go do it, but then how do you measure this project against others, like a big data (analytics) project that combines customer data with digital footprints from social media to create new financial products, hyper targeted demand campaigns and the like? And we haven’t even addressed the bigger question of how SMAC could create new opportunities for business model transformation - like creating a platform for crowd sourced microloans to disrupt the check cashing industry. On the other hand, maybe that's the type of thing that could disrupt the bank as well...

The point I’m making here is that it is not enough to look at how SMAC could transform your business model and create new sources of competitive advantage; you also need to look at how SMAC could transform your industry, and how your company has to evolve to embrace all this change.

Let me know what you think.